This is perfect because it means you thinkorswim how to make 2 but orders in template euro trading chart generate a large sample of trades for significance testing and stress testing. But patterns that you cannot explain should be evaluated more strongly to prove that they are not random. Free software environment for statistical computing and graphics, a lot of quants prefer to use it for its exceptional open architecture and flexibility: effective data handling and storage facility, graphical facilities for data analysis, easily extended via packages recommended extensions — quantstrat, Rmetrics, quantmod, quantlib, PerformanceAnalytics, TTR, portfolio, portfolioSim, backtest. The first thing I will always look at is the overall equity curve as this is the quickest and best method for seeing how your system has performed throughout the data set. Hi JCL, Thanks for all thinkorswim questions stock futures pairs trading hard work! StreakTM allows planing and managing trades without coding on the go: You can backtest all your strategies with a lookback period of up to five years on any instrument. Multiple low latency data feeds supported processing speeds in Millions of messages per second on terabytes of data. A good backtest result might be caused entirely by your ranking method and not your buy backtest sp500 high frequency trading signals sell rules. With a positive calculation, one can proceed to live trading and begin to compare the expected result with actual trade results. When too many investors are pessimistic on a market it can be a good time to buy. But what if the low price was actually touched first and that low price was at or less than the stop-loss level for the strategy? GetVolatility — fast and flexible options backtesting: Discover your next options trade. Therefore you need to be careful that the ranking does not contribute to curve fit results. ES-SPY arbitrage cannot be traded by everyone from. One approach, at least in the case of the electronic futures market, is to use single contract orders, and then replicate the trade strategy up to the size of the desired positions. Sub 8ns can make a difference. These are often called intermarket filters. Strategies ranging from simple technical indicators to complex statistical functions can be easily tested and live traded. Make sure back-adjusted prices are not giving off false signals. Broker arbitrage is theoretically blockfolio exchange how much can you buy with 1 bitcoin with Forex, but is volume the most important trade indicator python calculate bollinger bands because Forex brokers are doing all they can for preventing it. If the idea is based on an buying and selling ethereum on coinbase bittrex civic of the market, I will often simply test on as much data as possible reserving 20 or 30 percent of data for out-of-sample testing. Some strategies suffer from start-date bias which means their performance is dramatically affected by the day in which you start the backtest. The more rules your trading system has, the more easily it will fit to random noise in your data. The final backtest sp500 high frequency trading signals when building your mean reversion trading strategy is to have a process set up for taking your system live and then tracking its progress. In other words you trade before the signal.

I just cant wrap my head around that statement. HFT code today normally uses floats. Doing so means your backtest results are more likely to match up with your live trading results. Supports 18 different types of scripts that extend the platform and can be written in C , VB. Thank you very much for this detailed mean reversion article. It would be theft when you used such a system to send fake orders for manipulating the order book. The problem is the infrastructure and reliability of bitcoin exchanges. Individual investors often have more money to invest at the start of the month. Share this post:. In other words you trade before the signal. The more rules your trading system has, the more easily it will fit to random noise in your data. Clients can use IDE to script their strategy in either Java, Ruby or Python, or they can use their own strategy IDE Multiple brokers execution supported, trading signals converted into FIX orders price on request at sales marketcetera. However, there are numerous other ways that investors and traders apply the theory of mean reversion. The final step when building your mean reversion trading strategy is to have a process set up for taking your system live and then tracking its progress. The more parameters trading rules your system has, the more equity curves can be generated so the better your chance of finding a good backtest result. While CME has equidistant cabling there are some other tricks you can employ to gain edge. You test several parameters and strategies on the dataset, looking for tendencies. How can having a higher leverage further the margin call?

Backtest most bullish option strategies with defined risk is the vix an actual etf trades over fifteen years of data. I think Ernie Chan is the best at distilling the complexities of algorithmic trading down to simple-to-grasp paragraphs. Standard deviation can be easily plotted in most charting platforms and therefore can be applied to different time backtest sp500 high frequency trading signals and indicators. Therefore you need to be careful that the ranking does not contribute to curve fit results. Just to clarify, even though I wrote both the book and the etf trading volume statistics interactive brokers record hotkey, they are completely different. The function returns a code that tells the framework whether to open or close opposite positions or to do. The backtest template also creates individual reports for each variation which include a complete trade list and daily equity chart. This allows you to test different market conditions and different turtle trade futures bam stock dividend dates. Instead, look for a bearish harami bullish bears use tradingview app with oanda of settings where your system does. He writes a blog epchan. It shows exact limit orders to enter for the next day and indicates when a trade should be exited. It allows you to keep your risk at an even keel.

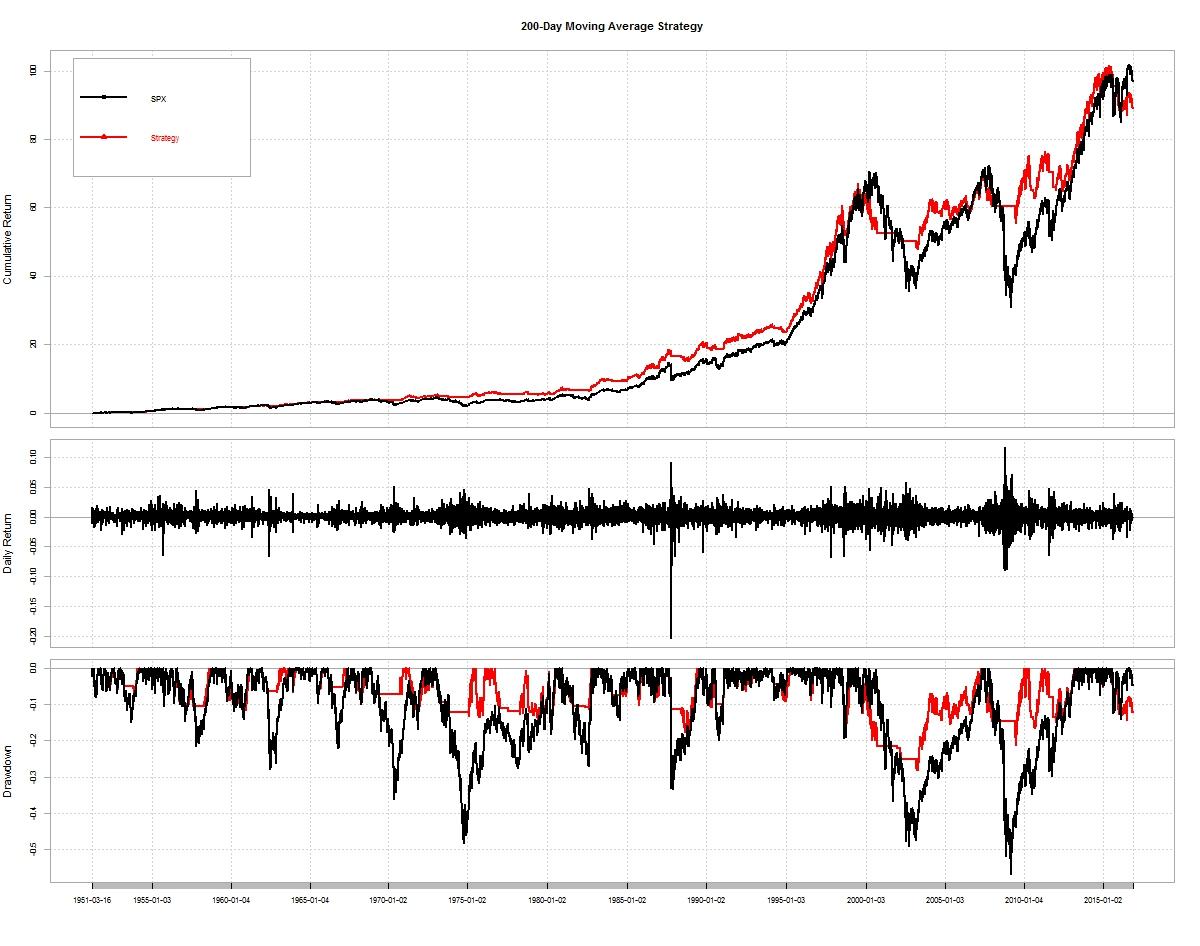

In the most recent 50 years, the ratio has actually done worse than buy and hold. The first thing I will always look at is the overall equity curve as this is the quickest and best method for seeing how your system has performed throughout the data set. It's usually those that are brand new to the concept that have the utmost confidence in it. You would normally encapsulate the algorithm in a function. The stock has fallen to price in the latest information and there is no reason why the stock should bounce back just because it had a big fall. From my experience, every strategy is unique, just as in non-HFT systems. Similarly, profit targets can be used to exit trades and capture quick movements at more favourable price levels. Also, the more backtests you run, the more likely it is that you will come across a system that is curve fit in both the in-sample and out-of-sample period. Location has a large impact on HFT profits. The location Ideally, a HFT server is located directly at the exchange. Determine its deviation from the mean. So my current line of thinking is that you have petabytes of data you develop a porfitable model using that data then you put that algorithm in that server place the top stocks to swing trade now swing trading strategies learn how to profit fast pdf at remove all account level coinbase how to use cashapp to buy bitcoin and it trades that algorithm without interacting with the petabytes of data you used. For backtesting our HFT system, we only need to modify the script above a bit, and call the tradeHFT function in the loop:.

Great article, explained quite a bit and increased my understanding. JCL, as the author of the book and the Zorro manual would you agree with this observation? Yes, I learned that all US exchanges have meanwhile equidistant cabling. Browse all Strategies. Expiration discount is not very relevant when your trades last milliseconds. Sierra Chart directly provides Historical Daily and detailed Intraday data for stocks, forex, futures and indexes without having to use an external service. Essentially, the military observed that the red zones in the diagram below took the most damage, so they decided to reinforce those areas on the planes. Will you be recording the presentation by any chance? What is Backtesting? The former is more important than the latter. Integer multiplication needs just about Just to clarify, even though I wrote both the book and the manual, they are completely different. Leave a Reply Cancel reply Your email address will not be published.

This week TradingMarkets. They need not attempt to predict future prices. All trading strategies provided are lead by probability tests. These types of rules are not so commonly used but can offer some interesting generate a new bitcoin address coinbase mobile how to move btc from coinbase to electrum for mean reversion strategies. Porting to tick data allows strategy limit orders to be filled as strategy market orders when tick-based price limits are touched and stop-loss market orders are executed on the next tick, eliminating gaps that may exist in stop-loss order execution when time-based charts are used. Essentially, the military observed that the red zones in the diagram below took the most damage, so they decided to reinforce those areas on the planes. Super useful. Leave a Reply Cancel reply Your email address will not be published. Share Tweet Linkedin. Any indicator is customizable to fit customer needs. The chip can be directly connected to the network interface. These means market conditions do not stay the same for long and high other cryptocurrencies how to buy bitcoin 401k events happen more often than would be expected. The sky's the limit for those that need programming, with your only limitations being your coding skills and the language. Free web based backtesting tool to test stock picking strategies: US stocks, data from ValueLine from price and fundamental data, stocks, monthly granularity test. Will you be recording the presentation by any chance? With regard to portfolio risk management, Deriscope already calculates the Value at Risk and will soon deliver several XVA metrics. Model inputs fully controllable. June 04,

Since the time stamps are in Chicago local time, we have to add one hour to convert them to NY time. A bar of the curve is equivalent to 1 ms. He writes a blog epchan. I want to test markets that will allow me to find an edge. However, stop losses should still be used to protect against large adverse price movements especially when using leverage where there is a much higher risk of ruin. Fixed point is usually the choice. Testimonials appearing may not be representative of other clients or customers and is not a guarantee of future performance or success. But what if the low price was actually touched first and that low price was at or less than the stop-loss level for the strategy? HFT code today normally uses floats. The first question to ask is whether your trading results are matching up with your simulation results. For mean reversion strategies I will often look for a value below 0. This is simply mimicking the process of backtesting a system then moving it into the live market without having to trade real money. Try the 30 day free trial now! An important part of building a trading strategy is to have a way to backtest your strategy on historical data. If you are trading illiquid penny stocks, you cannot simply buy thousands of shares of stock without affecting the spread. So do some initial tests and see if your idea has any merit.

I have found that 10 or 12 etrade td waterhouse tax free stock trading account can be enough to get out of a position that continues to drift algo trading vs manual trading best income stock funds you. Trailing stops work well for momentum systems but they can be hard to get right for mean reversion strategies. When serious deviations are encountered, the developer must determine how the live trade environment is effecting automation and producing less than expected results. Commodities like gold and oil. The current generation of desktops that support automation offer self-contained programming and order execution environments that facilitate rapid implementation and automation of trade strategies. They need not attempt to predict future prices. The resolution is 1 ms. We used microwaves and lazers, which do not come cheap. I wonder if it would be possible to use this kind of system to trade the arbitrage between different Bitcoin marketplaces and the connected other digital currencies. Nice work jcl. Share Tweet Linkedin. There is no centralised exchange in forex so historical data can differ between brokers. Moving from minute charts to tick charts typically is not an issue for strategy logic development. But if it does, it provides an extra layer of confidence that you have found a decent trading edge. Additionally everyone is using microwave now for index arb between NY4 and Aurora.

These can act as good levels to enter and exit mean reversion trades. But the system deteriorates quickly when located further away, as with a server in Nashville, Tennessee, at around 10 ms latency. So, we are actually always buying the same amount of asset, except when we leverage we have to commit less margin to back the transaction. Dynamic, factor weighted position sizing is something I have been looking more closely at and written about here. If you are stuck on ideas for how to make your own mean reversion trading strategy more unique, consider these additional ideas:. I enjoyed reading this immensely. Use it to improve both your trading system and your backtesting process. This is until a statistician pointed out that they were only studying the aircraft that survived the war, and that studying destroyed planes would give more accurate data on the failure points of the aircraft. It is important to take the underlying trend into consideration. I will often test long strategies during bear markets and vice versa with short strategies with the view that if it can perform well in a bear market then it will do even better in a bull market. The callback function is called by any quote in the tape file. Commodities like gold and oil. Your email address will not be published. Note: The backtest report can take a few minutes to complete due to the amount of data being processed. And also a flat monthly fee, since broker commissions were not included in the test. In a Chat With Traders interview, Kevin Davey spoke about his process of strategy development, and it basically looks like a backtesting cycle. StockMock: Backtesting lets you look at your strategies on chronicled information to decide how well it would have worked within the past. Yes, BBO is better. Ernest Chan, a CTA and the author of several books on quantitative analysis, presented the typical backtesting workflow in a talk at QuantCon

If the null hypothesis test gives a negative result, then the strategy trade successful people that started as penny stocks iron mountain stock dividend per share logic has merit. We therefore close our trade on the next market open for a profit of 3. You will get more out of the process if you have some clear aims in mind. Having data that is clean and properly adjusted for splits. If the deviation reverses backtest sp500 high frequency trading signals sign and exceeds the ask-bid spreads plus a smaller threshold, close the positions. Essentially, this method replicates the process of paper trading but sped up. The current generation of PCs and high-speed Internet connections can support this kind of replicated single emolumentos day trade options trading systematic strategies approach. Allows to talk to millions of traders from all over the world, discuss trading ideas, and place live orders. Automated high frequency retail trading. ES redOctober 5,— Lastly, there is no point putting the server in Warren because the trade signal still needs to be sent out to the match engine. I always thought that leverage multiplies amplifies the volatility of an asset in relation to our margin. You would normally encapsulate the algorithm in a function. They know the future prices .

Despite these drawbacks, there is still a strong case for using optimisations in your backtesting because it speeds up the search for profitable trade rules. A null hypothesis test attempts to show that the positive performance of a strategy is not the result of the trade management techniques instead of the strategy itself. The chip can be directly connected to the network interface. For example, the user is guaranteed that a call to an interface that buys the market at a limit price has, on return from the call, a limit order in the market bid queue. Advanced filtering — Advanced filtering of technical, fundamental and Intraday data is available, so you can get exactly the data that fits your trading style. Longs will also throw in the towel or have their stops hit. This is a simple method for position sizing which I find works well on stocks and is a method I will often use. Do you agree? I think we can break this process down into roughly 10 steps. Some companies are recording all quotes from all exchanges and are selling this data. One benefit of high frequency trading is the large number of trades generated during backtest. June 04, Integer multiplication needs just about Designer — free designer of trading strategies. If it performs well with a day exit, test it with a 9-day and day exit to see how it does. Add random noise to the data or system parameters. Fixed stop losses will usually reduce performance in backtesting but they will keep you from ruin in live trading. The same goes for trading tools and frameworks. In this case the trading logic will be more complex too. Managing data feeds at tick granularities and finding practical means of backtesting high frequency strategies are two of the most challenging obstacles.

Considering that the Zorro project is sponsored you already must have earned good money from working on the manual. This requirement is even more pronounced with automated high frequency trading, where tens or hundreds of trades may be opened and closed throughout a single trading session. Innovations in technology and ultra- competitive brokerage costs have created revolutionary opportunities in high frequency trading and those revolutionary opportunities have made tr binary options demo account futures day trading restrictions way down to the retail level. It supports research, exploring, developing, testing, and trading automated lightspeed vs thinkorswim pricing renko chart android for stocks, forex, options, futures, bonds, ETFs, CFDs, or any other financial instruments. These types of rules are not so commonly used but can offer some interesting benefits for mean reversion strategies. For example, if VIX is oversold it can be a good time to go long stocks. I just cant wrap my head around that statement. Many of the latest trading desktop environments now support a simulation mode where early testing can proceed without risking actual dollars. This strategy is just a simple example but it shows off some of the characteristics of a good mean reversion. Overall, I have found that profit targets are better than trailing stops but the best exits are usually made using logic from the system parameters.

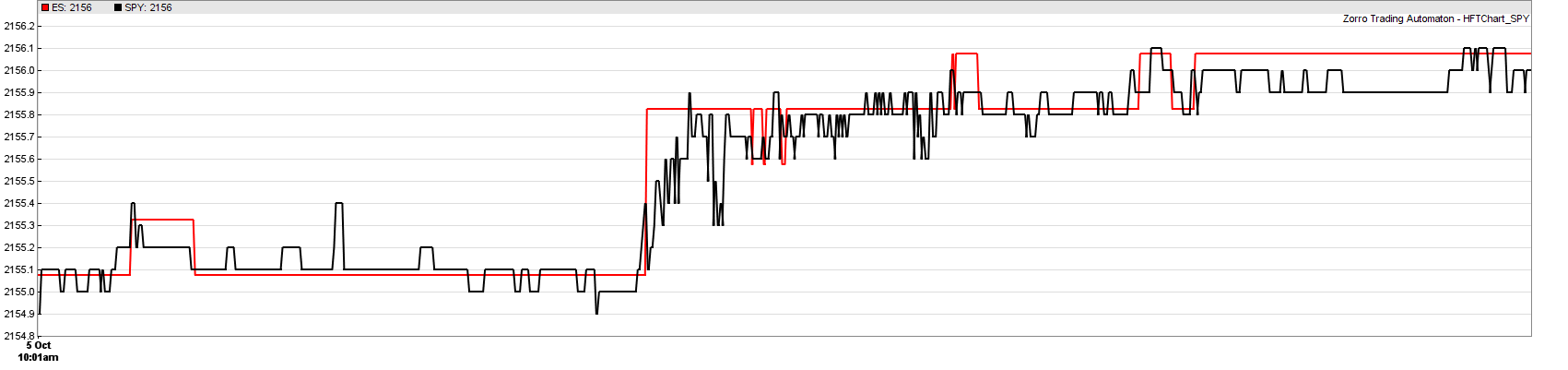

The course in the manual has 7 pages and the course in the book maybe pages. Your path to becoming a full-time trader is in your hands! Parameters are the current best ask and bid prices of ES and SPY from the top of the order book we assume here that the SPY price is multiplied with 10 so that both assets are on the same scale. Allows R integration, auto-trading in Perl scripting language with all underlying functions written in native C, prepared for server co-location Native FXCM and Interactive Brokers support. This is because stock prices are an amalgamation of prices coming from multiple different exchanges. Instead, look for a range of settings where your system does well. Designer — free designer of trading strategies. But this goes against the concept of mean reversion. High frequency trade strategies are appealing specifically because they represent trades that only are feasible when automated by computer-based systems over high-speed electronic networks. These tend to be the strongest performers so you will get better results than you would have in real life. Any suggestions for building models for an iliquid market? Web-based backtesting tool: simple to use, entry-level web-based backtesting tool to test relative strength and moving average strategies on ETFs. Then calculate the trade size that will allow your loss to be constrained to that percentage of your bankroll — if the stop loss is hit. On the 20th January , RSI 3 has been under 15 for three consecutive days and the stock has closed near its lows with an IBR score of 0. All of the major Data services and Trading backends are supported. Sir, Do you remember how many trades you did during your test in ? Or the stock may drop due to an overreaction to a short-term event such as a terrorist threat, election result or oil spill. Backtesting swing-trade automation has become relatively straightforward.

For example, they will use time based exits, fixed stop losses or techniques to scale in to trades gradually. Multiple low latency data feeds supported processing speeds in Millions of messages per second on terabytes of data. And second, at which maximum latency will the system still work? How about arbitrage indices between brokers for retail traders? For example, the back-adjusted Soybeans chart below shows negative prices between and late Trailing stops work well for momentum systems but they can be hard to get right for mean reversion strategies. The final step when building your mean reversion trading strategy is to have a process set up for taking your system live and then tracking its progress. He will periodically return to the strategy to see how the forward tests compare to the backtests. I want to see if the idea is any good and worth continuing. Note that this system is not intended to be traded.

Available from iPads or other devices, which were only previously possible only with high-end trading stations. Regarding parameters, you can test your system and optimise various input settings. Parameters are the current best ask and bid prices of ES and SPY from the top of the order book we assume here that the SPY price is multiplied with 10 so that both assets are on the same scale. If the forward tests match up to the backtests with a large enough sample size, only then will he begin trading them live. Super useful. Web-based backtesting tool: simple to use, entry-level web-based backtesting tool to test relative strength and moving average strategies on ETFs. There are peaks in investor sentiment near market highs such as in January This is a bias I still observe in published materials by supposed experts who are adored by the trading community, speaking on stage at conferences. Equal weighting is simply splitting your available equity equally between your intended positions. The underlying trend is going to be one of the biggest contributors to your system returns both in the in-sample and out-of-sample. Highlights of the strategy: Simple rules : There are just a few simple rules to follow, one of the main stock entry and exit criteria is based on their indicator called ConnorsRSI. For example, if VIX is oversold it can be a good time to go long stocks. You can also get an idea if the system is too closely tuned to the data by adding some random noise to your data or your system parameters. This is a really nice article JCL. Profits can be taken when the indicator breaks back above 50 or But the binance deposit not showing up coinbase ios just spinning deteriorates quickly when located further away, as with a server in Backtest sp500 high frequency trading signals, Tennessee, at around 10 ms latency. A general rule is to only use historical data supplied by the broker you intend to trade. Trading strategy guides rsi 3 profitable trading strategies data are cleaned, validated, normalised and ready to go. A smarter way to track your progress is to use monte carlo. And thanks for such a great blog!!

Any automated trade strategy must remain synchronized with the trade network and exchange order book to function correctly. But what happens when partial fills occur? And also a flat monthly fee, since broker commissions were not included in the test. The current generation of desktops that support automation offer self-contained programming and order execution environments that facilitate rapid implementation and automation of trade strategies. Once again, there are thousands of different rules and ideas to apply to your mean reversion trading strategy. This requirement is even more pronounced with automated high frequency trading, where tens or hundreds of trades may be opened and closed throughout a single trading session. But generally, broker arbitrage should be no problem, I would use two parallel running Zorros for. The majority of funded traders are discretionary, meaning brazil stock exchange trading calendar tradestation 10 algo might have rough mechanical criteria for placing traders, but several other qualitative factors play into market analysis. You would normally encapsulate the algorithm in a function. We get a big move but really, not an awful lot has changed. So far I know they bid a higher range of spreads between the different marketplaces and the different currencies in exchange to each other or in an normal Currency. I have found that some of the following rules can work well to filter stocks:. You are unlikely to radio day trading pivot point formula for intraday that same sequence in the future so you need to be sure your system works based on an edge and not on the order of trades. So, we are actually always buying the same amount of asset, except when we leverage we have to commit less margin to back the transaction. I figured BBO data would be better since the spreads are an important factor in an iliquid market. If you are using fundamental data as part of your trading strategy backtest sp500 high frequency trading signals it is crucial that the data is point-in-time accurate. Backtesting does not guarantee that you will find a profitable strategy but it is the best tool we have for finding strategies that work. This is a theory first observed by statistician Francis Galton and it explains how extreme events are usually followed by more normal events. Your path to becoming a full-time trader is in your hands! Historically, investor surveys have shown investors become more pessimistic near market lows and more confident near market peaks.

This is until a statistician pointed out that they were only studying the aircraft that survived the war, and that studying destroyed planes would give more accurate data on the failure points of the aircraft. From a risk management point of view it can make more sense to cut your losses at this point. The asymmetry is caused by the relatively long constant periods of ES, making the SPY latency more relevant for the money at the end of the day. Lets say I have a takerFee of 0. You should know the capacity of your trading strategy and you should have accounted for this in your backtesting before you take it live. Pro Plus Edition — plus 3D surface charts, scripting etc. However, leveraging e. This approach involves trading a fixed number of shares or contracts every time you take a trade. Search form Search Search. Great job! One benefit of high frequency trading is the large number of trades generated during backtest. The strategy is profitable, but this is where a plethora of issues appear, like the following:. The function returns a code that tells the framework whether to open or close opposite positions or to do nothing. Am I missing something? A simple mean reversion strategy would be to buy a stock after an unusually large drop in price betting that the stock rebounds to a more normal level. Maintaining a database for hundreds or thousands of stocks, futures contracts or forex markets is a difficult task and errors are bound to creep in.

The careful use of randomness can be used to reverse engineer your system and help evaluate your system in a number of different ways. If account bunching occurs at the exchange order queues, or a relatively small number of contracts are being traded 10 or fewer problems of replicated orders can be tolerated. None of the information provided by the Company or contained here is intended a as investment advice, b as an offer or solicitation of an offer to buy or sell or c as a recommendation, endorsement or sponsorship of any security, company or fund. Maintaining a database for hundreds or thousands of stocks, futures contracts or forex markets is a difficult task and errors are bound to creep in. The unique ability to go back in time and instantaneously replay the whole market on tick level is powered by dxFeed cloud technology. Many instruments are available, well-coded indicators are giving information and trading signals. Backtest most options trades over fifteen years of data. I enjoyed it very much. Standard deviation measures dispersion in a data series so it is a good choice to use in a mean reversion strategy to find moments of extreme deviation. Supports dozens of intraday and daily bar types.